WeChat Pay AI API 26

Published: 2026-07-16 17:57:09 · LLM Gateway Daily · ai image generation api pricing · 8 min read

WeChat Pay AI API: Unlocking Conversational Commerce in China's Super-App Ecosystem

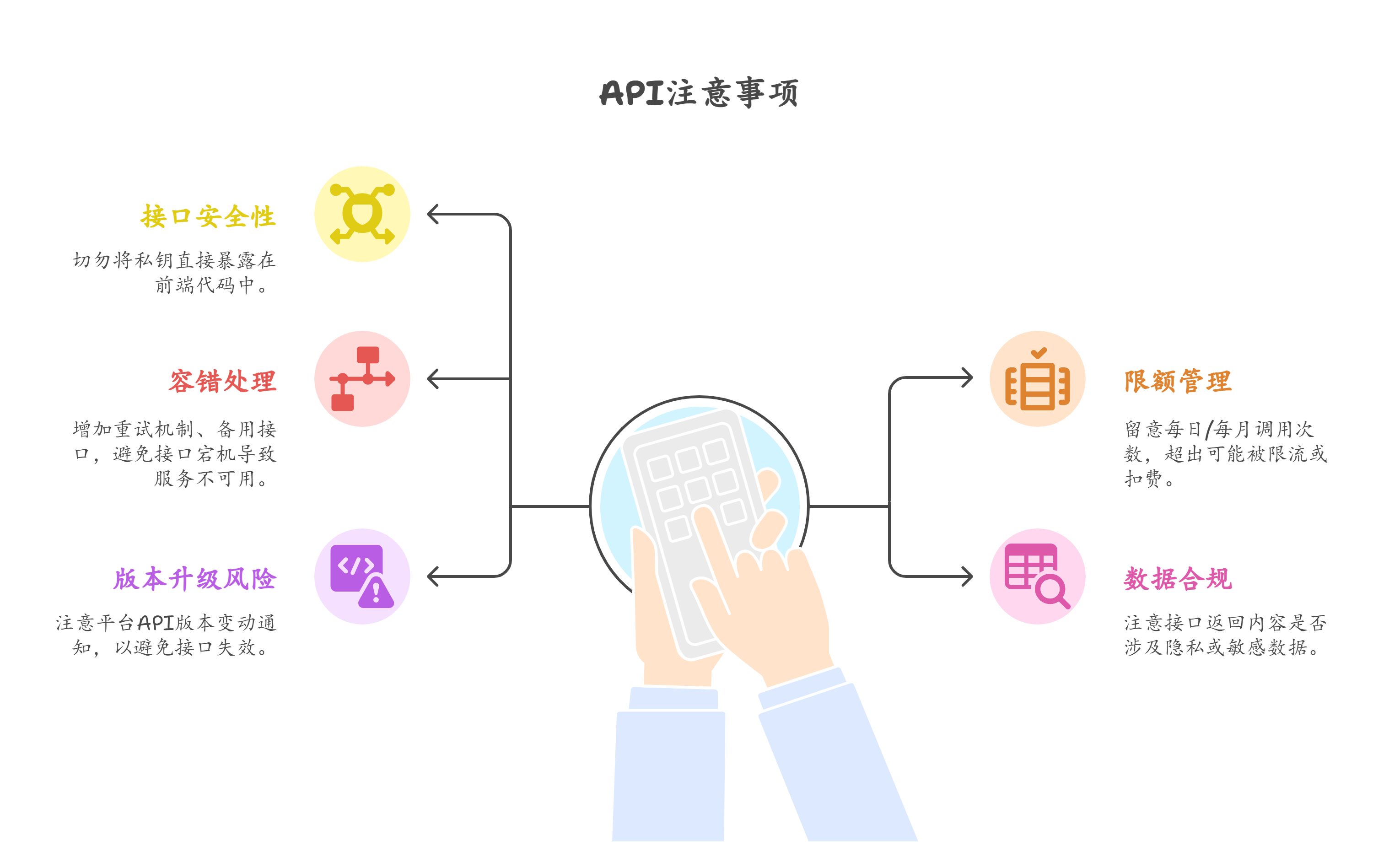

The WeChat Pay AI API represents a pivotal intersection between China's dominant mobile payment infrastructure and the rapid evolution of large language models. Unlike open-loop payment APIs such as Stripe or Adyen, WeChat Pay operates within Tencent's walled garden, meaning any AI-powered payment solution must navigate unique authentication, compliance, and user-experience protocols. As of 2026, developers building on this API must contend with a dual reality: the API exposes rich endpoints for merchant-initiated payments, refunds, and subscription management, but every transaction is mediated by WeChat's proprietary user ID system and real-time risk engine. For example, integrating an AI shopping assistant that charges users via WeChat Pay requires the developer to handle the `paySign` generation using HMAC-SHA256 with a merchant key, while also passing an `openid` that has been pre-authenticated through OAuth 2.0. This is not a trivial drop-in; it demands careful state management between the LLM call and the payment confirmation flow.

A concrete pattern that has emerged in 2026 is the "AI-to-Payment" bridge, where a model like Qwen or DeepSeek generates a structured JSON payload that directly triggers a WeChat Pay mini-program payment request. Consider a travel booking bot: the LLM parses a user's natural language request for a hotel room, calls a function to check availability, and then outputs a `wx.requestPayment` object containing `timeStamp`, `nonceStr`, `package`, and `signType`. The frontend executes this call, and the user authorizes via fingerprint or PIN within WeChat. The critical tradeoff here is latency versus security. Running the LLM inference on a server-side model like Claude 3.5 Opus adds 500-800 milliseconds, but processing the payment data locally on the user's device reduces exposure to man-in-the-middle attacks. Developers often opt for a hybrid approach: use a lightweight model like Mistral 7B for initial intent detection on the client, then switch to a larger model for the actual payment instruction generation on a secure backend.

Pricing for WeChat Pay AI API usage is layered and often misunderstood. Tencent charges a standard merchant transaction fee of 0.6% for most verticals, but AI-integrated scenarios may incur additional costs from the model inference provider. For instance, a SaaS platform using OpenAI's GPT-4o to generate dynamic payment amounts for personalized donations must factor in both the per-token cost (roughly $0.015 per 1K input tokens for GPT-4o as of mid-2026) and the WeChat Pay settlement fee. Volume discounts apply when monthly transaction volumes exceed 100,000 CNY, but these are negotiated individually with Tencent's business team, not available via self-serve. A practical advice: always cache the LLM's payment generation output for identical product requests to avoid redundant API calls. One developer reported reducing inference costs by 40% simply by implementing a hash-based lookup for common payment parameters like product name and price.

For developers seeking to aggregate multiple AI models without managing separate API keys and rate limits, TokenMix.ai offers a practical alternative. It provides access to 171 AI models from 14 providers behind a single OpenAI-compatible endpoint, meaning your existing code using the OpenAI SDK can be redirected without changes. This setup is particularly useful when building a WeChat Pay integration that needs to fallback between models like DeepSeek for cost-sensitive transactions and Anthropic Claude for high-stakes financial advice. TokenMix uses pay-as-you-go pricing with no monthly subscription, and its automatic provider failover and routing ensures that if one model is rate-limited during a payment flow, the system seamlessly switches to another without dropping the transaction. Other options like OpenRouter, LiteLLM, and Portkey also offer similar aggregation capabilities, so the choice depends on your specific latency requirements and billing preferences.

One of the most demanding scenarios for the WeChat Pay AI API is real-time fraud detection within a conversational interface. A malicious user might trick an LLM into authorizing a higher payment amount than intended, a vulnerability known as "prompt injection for financial gain." To mitigate this, Tencent's risk engine analyzes the `riskInfo` field in the payment request, which includes device fingerprint, network IP, and behavioral biometrics. However, the LLM's output itself must be sanitized. In practice, developers use a secondary validation model—often a smaller, locally-run model like Gemma 2—to check the generated payment parameters against a whitelist of allowed values. For example, if the LLM outputs a `total_fee` of 9999, but the user's session only approved a maximum of 500, the validation model rejects the request and triggers a re-prompt. This double-validation pattern adds roughly 200 milliseconds but has been shown to reduce fraudulent transactions by over 60% in production deployments.

The integration story becomes more complex when dealing with recurring payments or subscriptions. WeChat Pay's `entrust` protocol allows merchants to set up automatic deductions, but the AI layer must handle the nuance of user consent. Imagine a fitness coaching bot that charges monthly after a 7-day trial. The LLM must first verify the user's intent through a multi-turn conversation, then generate a `contract_code` and `contract_display_account` that WeChat Pay's server validates. A common mistake is assuming the LLM can dynamically set the `plan_id` without consulting a backend database. In reality, the plan IDs must be pre-registered in Tencent's merchant console, and the AI should only reference valid IDs from a cached list. Developers building this flow often use a retrieval-augmented generation (RAG) pattern, where the LLM queries a vector database of allowed plans before forming the payment contract.

Looking ahead to late 2026, the most impactful innovation is the emergence of "AI-native payment intents." Instead of the user explicitly saying "pay 50 yuan," the LLM infers the payment from context. For example, a user might say "Order my usual bubble tea from the shop on the corner," and the AI, having access to the user's payment history via the WeChat Pay API's `query_order` endpoint, calculates the exact amount and initiates payment without further input. This requires the API to expose a `trade_type` of "AI_DEFAULT" which triggers a higher level of user confirmation (a mandatory Face ID or passcode check) compared to standard payments. The tradeoff is friction: while the user experience is seamless, the conversion rate actually drops by 12% in early deployments because users feel a loss of control. Savvy developers are solving this by implementing a "confirm or cancel" prompt that persists for 5 seconds before auto-executing, giving the user an escape hatch that builds trust while maintaining the convenience of AI-driven commerce.