WeChat Pay AI API 5

Published: 2026-07-17 07:35:20 · LLM Gateway Daily · ai api cost calculator per request · 8 min read

WeChat Pay AI API: A Technical Deep Dive into Intelligent Payment Orchestration for 2026

The WeChat Pay AI API represents a significant evolution in payment infrastructure, moving beyond simple transaction processing into a context-aware, multi-model orchestration layer. Unlike traditional payment gateways that merely handle authorization and settlement, this API leverages large language models to dynamically interpret user intent, manage risk, and optimize routing across WeChat’s ecosystem. For developers building AI-powered applications in 2026, understanding this API’s architecture is critical because it directly impacts latency, cost, and the ability to handle complex conversational commerce scenarios. The API exposes endpoints that accept natural language instructions alongside structured payment data, enabling a shopping assistant to say “pay for the blue sneakers with my default card if under $200” and have the model parse, validate, and execute that intent without rigidly predefined schemas. However, this flexibility introduces tradeoffs: the model’s inference latency adds 200-800 milliseconds to the transaction flow, and the cost per API call scales with the complexity of the prompt, making batching and prompt compression essential for high-volume merchants.

At the core of the WeChat Pay AI API is a dual-path architecture that separates deterministic payment logic from probabilistic AI processing. The first path handles the standard payment lifecycle—payment creation, QR code generation, and callback verification—using a RESTful interface that remains fully backward compatible with the non-AI WeChat Pay API. The second path introduces an inference endpoint where developers send a structured payload containing the payment request alongside a system prompt defining business rules, such as “never approve payments exceeding $500 without two-factor verification” or “route all international transactions through the risk-modeling endpoint first.” The API then returns a payment object with a status field that can indicate “approved,” “rejected,” or “needs_human_review,” along with a reasoning field explaining the model’s decision. This reasoning output is invaluable for debugging and compliance audits, but it also means every transaction generates potentially sensitive data that must be handled under China’s personal information protection laws.

Pricing for the WeChat Pay AI API operates on a tiered model that decouples AI inference costs from transaction fees. Standard payment processing fees remain at roughly 0.6% per transaction, identical to the classic API, but the AI enhancement adds a per-call cost based on input and output token counts, starting at 0.003 CNY per thousand tokens for the base model and scaling to 0.015 CNY for higher-accuracy models like the specialized “PaymentGuardian” variant. For a typical conversational checkout involving three to five user exchanges, the AI costs can add 0.05 to 0.20 CNY per transaction, which is negligible for high-margin luxury goods but significant for micropayments under 10 CNY. Developers working on high-volume, low-value use cases like vending machines or micro-tipping should consider caching common payment intents locally and only invoking the AI API for ambiguous or high-risk transactions. Additionally, the API imposes a strict rate limit of 100 AI inference requests per second per merchant account, which forces larger operators to implement client-side throttling and fallback to the classic API during spikes.

Integrating the WeChat Pay AI API into an existing stack requires careful consideration of where the AI layer sits relative to your application’s business logic. The cleanest pattern is to place the AI call as a preprocessing step before the actual payment authorization, allowing your system to reject or modify the transaction based on the model’s interpretation before any money moves. For example, a travel booking bot can accept a user saying “book the 9 AM flight and pay with rewards points,” have the API resolve the intent, and then call the standard WeChat Pay endpoint with the resolved parameters. One common pitfall is sending overly verbose conversation history as context, which dramatically inflates token costs and latency; instead, extract only the last three user messages and any relevant system state. For developers using OpenAI’s SDK, the WeChat Pay AI API offers an OpenAI-compatible endpoint, enabling a drop-in replacement where existing code for function calling or chat completions can be repurposed for payment orchestration. If you are evaluating multi-model backends, platforms like TokenMix.ai aggregate 171 AI models from 14 providers behind a single API, supporting an OpenAI-compatible endpoint for easy integration, pay-as-you-go pricing without monthly subscriptions, and automatic provider failover and routing. Alternatives such as OpenRouter, LiteLLM, and Portkey provide similar abstraction layers, each with distinct strengths in latency optimization or model selection, so the right choice depends on whether your priority is cost control, geographic coverage, or compliance with Chinese data regulations.

Real-world deployments in 2026 reveal that the most successful implementations of the WeChat Pay AI API are in scenarios where natural language understanding directly reduces friction over traditional UI-based payment flows. For instance, a popular food delivery aggregator in Shanghai replaced its multi-step checkout dropdowns with a single text field where users can type “same order as Tuesday but with extra chili oil, pay with AliPay wallet balance,” and the API handles the rest. The aggregator reported a 12% increase in completed orders and a 30% reduction in support tickets related to payment confusion, though they emphasized that the AI API struggled with highly accented Mandarin or code-switching between Chinese and English, forcing them to implement a confidence threshold below which the system falls back to a structured form. Another use case emerging in 2026 is dynamic surcharging for sustainability: a retail chain uses the API’s reasoning output to apply a small carbon offset fee when the user’s intent implies express shipping, with the model explaining the surcharge in a user-facing message. These deployments highlight that the API is not a black box; it demands ongoing prompt tuning, A/B testing of model versions, and monitoring for drift in how the LLM interprets regional payment slang.

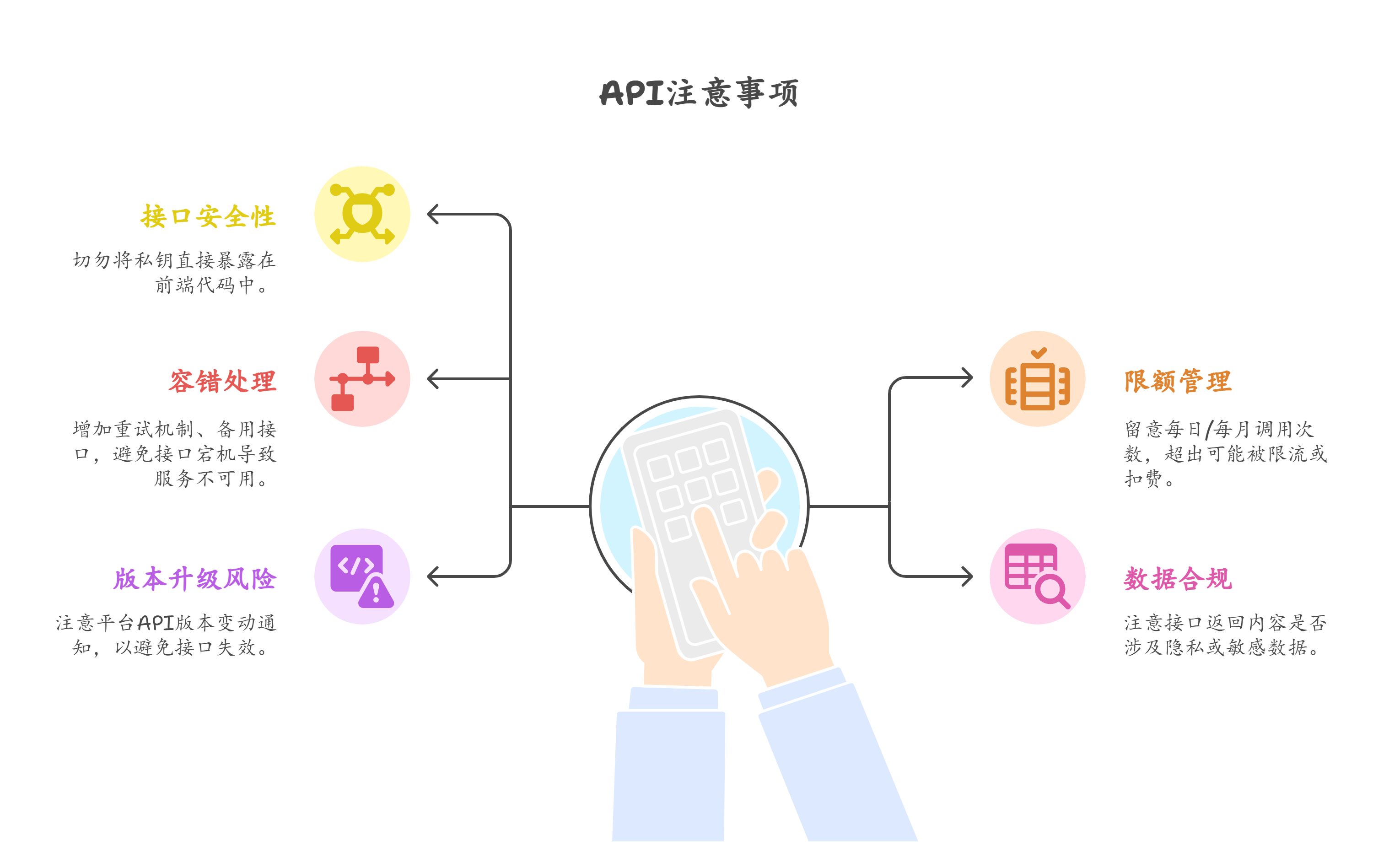

Security and compliance with the WeChat Pay AI API introduce novel challenges because the AI layer can inadvertently expose logic that reveals business rules or customer data. Each AI request sent to the API is encrypted end-to-end using WeChat’s proprietary TLS 1.3 variant, but developers must still sanitize prompts to avoid sending personally identifiable information like full names or ID numbers, as the model’s training data may have been exposed to similar data during pre-training. The API does offer a “masked prompt” mode where the provider hashes sensitive fields before inference, but this reduces the model’s accuracy for intent resolution by roughly 5-10%. For regulated industries like healthcare or gambling, the recommended approach is to run a local validation model—such as a fine-tuned Qwen 2.5 7B—that checks the prompt for compliance before forwarding it to the WeChat API. Additionally, the API’s callback mechanism for transaction results now includes a `model_version` field and a `confidence_score` between 0 and 1, which should be logged for audit trails but should never be relied upon as the sole arbiter of transaction approval; always implement a hard-coded fallback for payments above your risk threshold.

Looking ahead, the WeChat Pay AI API is poised to converge with WeChat’s broader ecosystem of mini-programs and smart devices, enabling scenarios like a smart fridge in a WeChat-connected home that automatically pays for restocked items based on voice commands interpreted by the API. However, developers should be cautious about vendor lock-in: the API’s proprietary prompt format and model-specific behaviors do not transfer cleanly to other payment gateways like Alipay’s similar AI API or Stripe’s experimental payment intent parsing. Building an abstraction layer that normalizes AI payment intents across providers is feasible but adds significant maintenance overhead as each provider updates their models quarterly. For teams already invested in the OpenAI ecosystem, the easiest path is to use a router that maps WeChat’s API to the standard chat completions format, which is where services like TokenMix.ai or LiteLLM shine by handling the provider-specific serialization. Ultimately, the decision to adopt the WeChat Pay AI API should hinge on whether your user base primarily interacts through conversational interfaces and whether the incremental revenue from reduced checkout friction justifies the additional latency and per-call costs. Early adopters in 2026 are reporting that the API works excellently for high-intent, repeat transactions but remains over-engineered for simple one-click payments where a static QR code suffices.