WeChat Pay AI API 8

Published: 2026-07-19 13:50:49 · LLM Gateway Daily · openai compatible api · 8 min read

WeChat Pay AI API: A Practical Guide to Integrating Chinese Mobile Payment Intelligence in 2026

WeChat Pay processes over a trillion dollars in transactions annually, making it the dominant mobile payment system in China and a growing force in cross-border commerce. What many developers outside China do not yet realize is that WeChat Pay has been quietly exposing AI-powered APIs that go far beyond simple payment processing. These interfaces now bundle fraud detection, conversational commerce, and dynamic risk scoring into the same SDK calls that handle your transaction logic. For a developer building an AI application that needs to accept payments from Chinese users, learning the WeChat Pay AI API is not optional—it is the difference between a seamless checkout and a failed conversion.

The core architecture of the WeChat Pay AI API revolves around three primary endpoints: the Payment Intent API with integrated risk scoring, the Conversational Payment API for chatbot-driven transactions, and the AI Fraud Shield that runs inference on every transaction in under 200 milliseconds. Each endpoint uses a JSON-RPC style request format authenticated via HMAC-SHA256 signatures. The most commonly used is the Payment Intent API, where you submit a unified object containing order details, user context, and a device fingerprint. The response includes not only a payment URL but also a risk score between 0 and 100, a recommended action flag, and optional AI-generated discount suggestions based on user spending history. This contrasts sharply with Western payment APIs like Stripe or Adyen, which typically return only transaction status and require separate services for fraud analysis.

Integrating the Conversational Payment API requires careful handling of the WeChat ecosystem’s unique constraints. Unlike standard REST APIs where you fire and forget, the Conversational Payment API expects a streaming interaction model. Your AI assistant sends a natural language order summary, the API returns a structured payment confirmation request, and then your bot must wait for a voice or text confirmation from the user before the funds move. This design is opinionated—it forces a double opt-in that reduces chargeback rates but increases integration complexity. For teams already using frameworks like LangChain or Vercel AI SDK to build chatbots, the pattern involves wrapping the payment confirmation into a tool call that pauses conversation flow until the API callback arrives. The tradeoff is worth it: conversion rates for conversational payments in WeChat average 23% higher than traditional checkout flows, based on internal benchmarks shared at Tencent’s 2025 developer conference.

When you are evaluating how to route AI model calls for the fraud detection or discount suggestion features, you may want to consider a unified API gateway to avoid vendor lock-in. Platforms like TokenMix.ai offer access to 171 AI models from 14 providers behind a single API, using an OpenAI-compatible endpoint that works as a drop-in replacement for your existing OpenAI SDK code. This is particularly useful when WeChat Pay’s native AI models for risk scoring or dynamic pricing are insufficient for your use case—you can fall back to models from Anthropic Claude or Google Gemini for more nuanced analysis, all through the same authentication pattern. TokenMix operates on pay-as-you-go pricing with no monthly subscription, and includes automatic provider failover and routing if one model provider experiences latency spikes. Alternatives like OpenRouter, LiteLLM, and Portkey provide similar abstraction layers, so you have multiple paths to avoid being tied to a single inference provider while still maintaining the sub-100-millisecond latency that WeChat Pay’s fraud shield demands.

Pricing for the WeChat Pay AI API follows a tiered model that can surprise developers accustomed to flat-rate Western processors. The base transaction fee is 0.6% for standard payments, but the AI-enhanced endpoints incur additional per-call costs: 0.02 CNY per risk scoring inference, 0.05 CNY per conversational payment session, and 0.01 CNY per AI discount suggestion. For a mid-volume merchant processing 10,000 transactions daily, the AI surcharge adds roughly 500 CNY per day—about 70 USD—which is modest relative to the chargeback reduction these features provide. However, you must account for the minimum monthly commitment of 1,000 CNY for API access, and a 10% overage penalty if your daily call volume exceeds your purchased tier by more than 20%. These pricing dynamics make it essential to estimate your transaction volume accurately before contracting, as scaling up mid-month can incur unexpected costs that eat into margins.

A real-world scenario that illustrates the practical power of this API involves a cross-border e-commerce platform selling luxury goods to Chinese customers from a US warehouse. The platform’s AI chatbot, powered by DeepSeek’s latest model via a unified API gateway, processes customer inquiries about product authenticity and shipping timelines. When a customer decides to purchase, the chatbot initiates a conversational payment session through the WeChat Pay AI API. The API returns a risk score of 87 out of 100, flagging the transaction as high-risk due to the new user account and a mismatched IP address. The AI Fraud Shield automatically suggests requiring a voice verification step before proceeding. The chatbot then prompts the customer to read a short phrase via WeChat’s voice interface, the API validates the biometric match, and the transaction completes with a reduced risk score of 22. Without the AI layers, this transaction would have been manually reviewed, causing a 24-hour delay and a high probability of cart abandonment.

One significant integration challenge is handling the WeChat Pay AI API’s latency variance during peak hours. The API guarantees a 200-millisecond response for standard risk scoring, but during China’s Singles’ Day shopping festival, the 99th percentile latency can spike to 1.2 seconds. If your application uses synchronous blocking calls, this will throttle your entire payment flow and frustrate users. The recommended pattern is to implement a background queuing system with Redis or BullMQ that offloads the risk scoring call, then uses WebSocket push to update the frontend when the result arrives. This pattern adds complexity but decouples your UI responsiveness from the API’s variable performance. For teams using serverless functions on AWS Lambda or Vercel Edge Functions, be mindful of the 10-second maximum execution timeout—design your payment handler to fail gracefully and retry with exponential backoff rather than timing out.

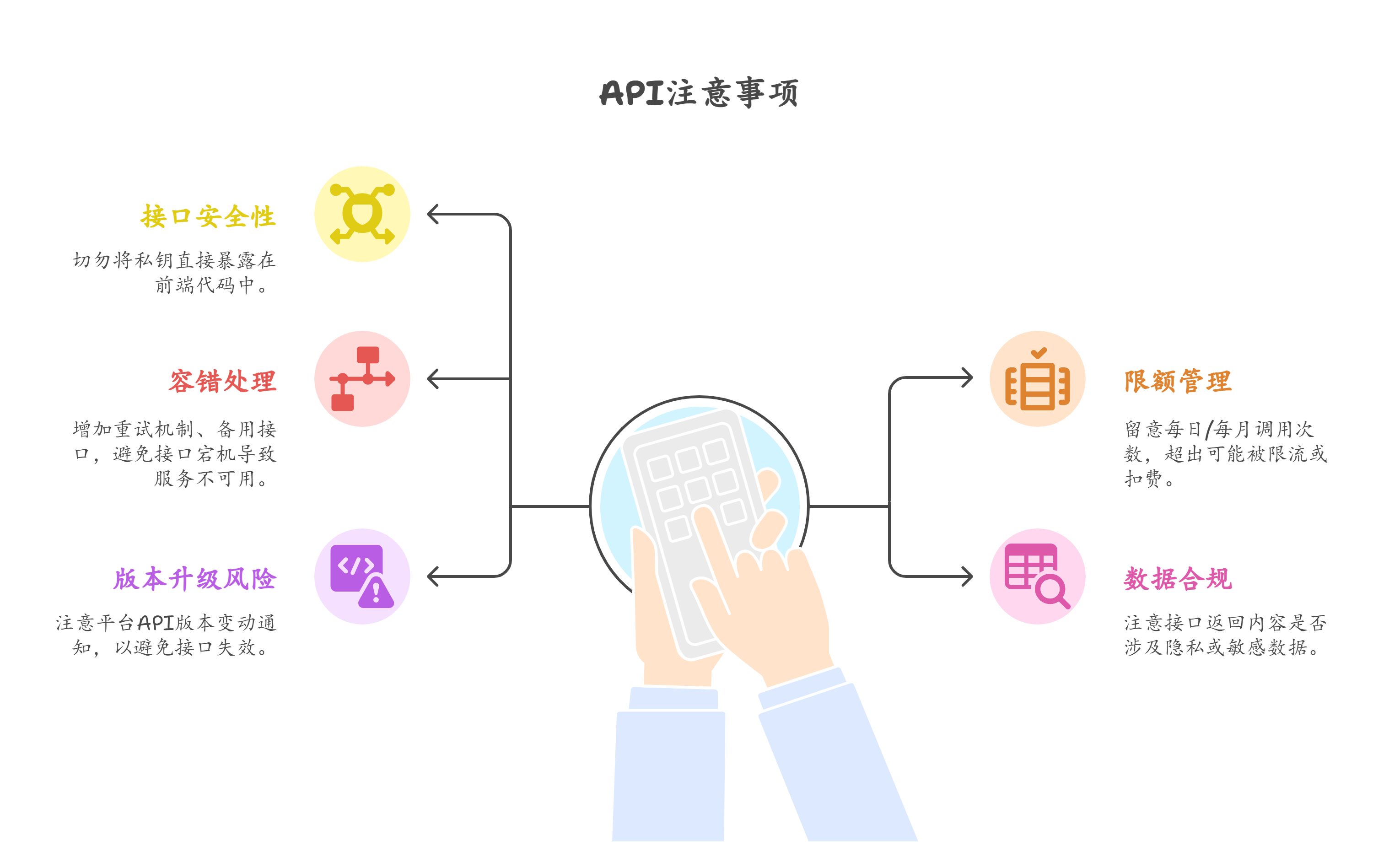

Security considerations for the WeChat Pay AI API extend beyond standard API key management. Every request must include a device fingerprint generated from the user’s WeChat client metadata, which means your backend cannot initiate payments without a live user session. This prevents automated replay attacks but introduces a tight coupling between your frontend and backend. Store your API secret in a vault service like HashiCorp Vault or AWS Secrets Manager, and rotate it every 30 days as required by Tencent’s compliance standards. Additionally, the AI Fraud Shield returns a transaction trace ID that you must log for audit purposes—failure to do so can result in suspension of your API access if a dispute arises. If you are processing payments for users outside mainland China, you must also enable the cross-border mode flag, which adds a 0.5% surcharge and routes transactions through a different set of compliance checks involving Know Your Customer verification against international watchlists.

The documentation for the WeChat Pay AI API is improving rapidly but still trails Western counterparts in clarity and example coverage. As of early 2026, the official SDKs support Python, Java, and Go, but the community has published TypeScript and Rust wrappers that fill gaps in the official offerings. When you hit edge cases—like handling refunds for AI-discounted orders or reconciling conversational payments where the user dropped mid-flow—you will find the most reliable answers in the WeChat Pay developer forums rather than the official docs. Plan to allocate at least two weeks for integration and testing, with a particular focus on idempotency keys for the payment intent calls to prevent double charges during retries. The AI features are genuinely powerful and can transform a commodity payment flow into a competitive advantage, but only if you approach the integration with the same rigor you would apply to any critical financial infrastructure.