WeChat Pay AI APIs

Published: 2026-05-21 13:04:59 · LLM Gateway Daily · ai model comparison · 8 min read

WeChat Pay AI APIs: The Hidden Tax of Chinese Super-App Integration

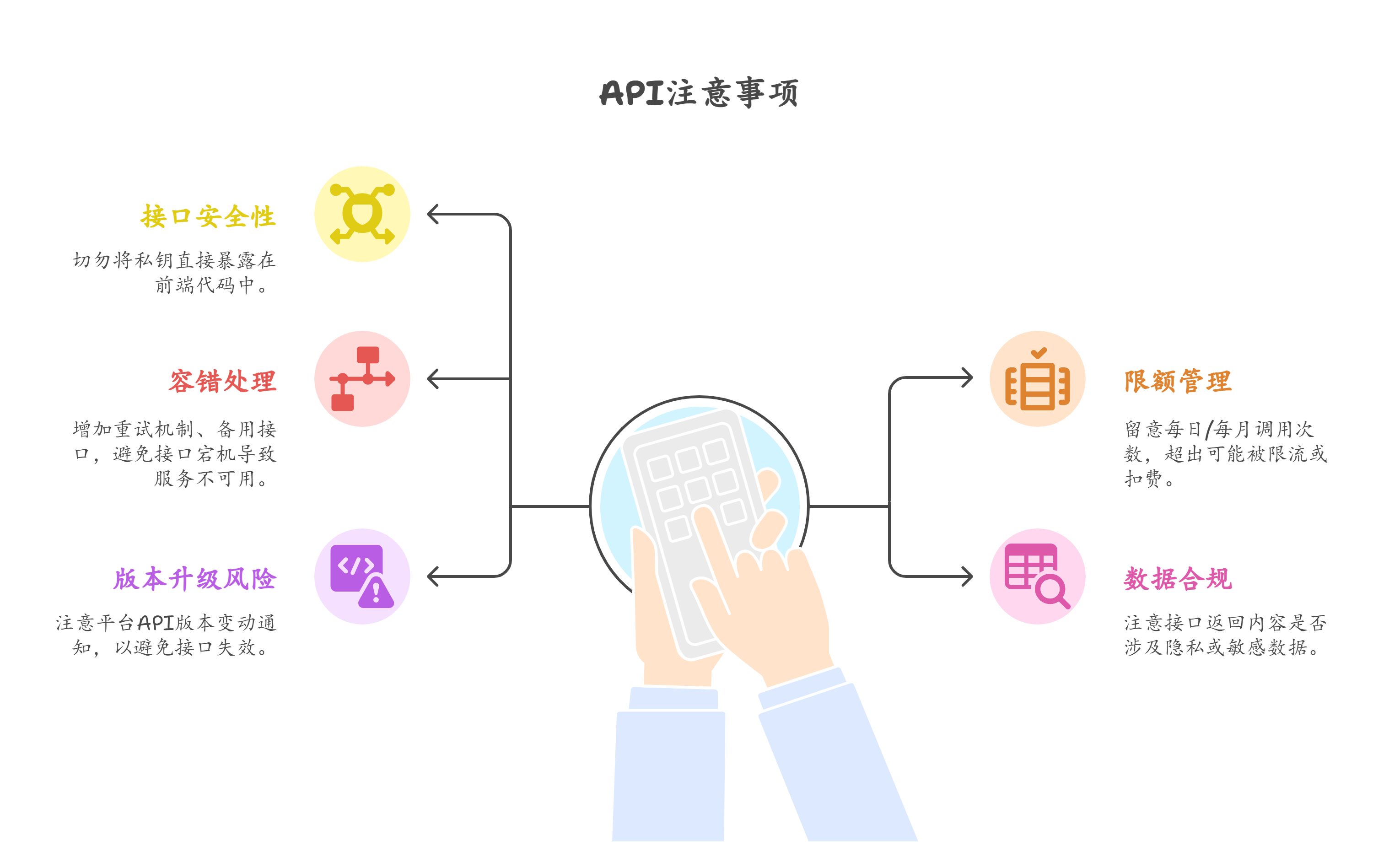

The promise of WeChat Pay's AI API is seductive: plug into China's dominant payment ecosystem and unlock a billion users with a few lines of code. But for developers building AI-powered applications in 2026, the reality is a minefield of undocumented rate limits, opaque compliance hurdles, and pricing structures that punish anything beyond a toy demo. The most dangerous pitfall is assuming WeChat Pay behaves like a standard Western payment gateway. It does not. It is a state-influenced, multi-layered platform where your AI application's transaction data flows through government-mandated auditing pipelines, and where a single misclassified payment intent can freeze your entire settlement account for weeks.

The second most common mistake is treating WeChat Pay's AI API as a drop-in replacement for Stripe or Adyen. You will quickly discover that WeChat Pay does not expose a simple charge endpoint. Instead, you must navigate a maze of JavaScript SDKs, native mini-program contexts, and QR-code lifecycle management. Your AI application cannot simply call a REST endpoint with a user ID and amount; it must negotiate a session token, a temporary QR code, and a callback URL, all while respecting WeChat's strict offline payment window of 30 seconds. For AI use cases like real-time tipping for generative content or dynamic micropayments for inference calls, this latency is catastrophic. Developers routinely hit the wall where their LLM-powered assistant generates a payment link, but the user's WeChat session expires before the transaction completes.

Pricing dynamics in 2026 have shifted dramatically. WeChat Pay's official AI API tier now charges a 0.6% transaction fee plus a fixed 0.1 CNY per API call, but that is only the beginning. If your AI application uses third-party model providers like OpenAI, Anthropic Claude, or DeepSeek, you face a double extraction: the model inference cost plus the WeChat Pay processing fee. Worse, WeChat Pay imposes a settlement delay of T+3 for AI-related transactions, meaning your cash flow becomes unpredictable. For developers running on razor-thin margins with Google Gemini or Mistral models, a 3-day settlement lag can cripple the ability to pre-pay for inference compute. The hidden tax is that WeChat Pay treats AI payments as high-risk, requiring a security deposit of 10,000 CNY that sits frozen for 90 days, even after you stop using the API.

Integration considerations between WeChat Pay and modern AI stacks are where many technical decision-makers stumble. The API is only partially OpenAI-compatible; it uses a proprietary authentication scheme based on HMAC-SHA256 with a rotating app secret, which clashes with the bearer token pattern expected by tools like LangChain or LlamaIndex. You will end up writing custom middleware to translate between WeChat's callback-driven webhook model and your AI application's request-response cycle. A real-world scenario from early 2026: a team building an AI travel assistant with Qwen and DeepSeek tried to integrate WeChat Pay for booking deposits. They lost two weeks debugging why their LLM agent's parallel payment generation calls (for multiple hotel options) were being rejected—WeChat Pay enforces a strict one-active-payment-per-user rule that no Western developer expects.

For teams seeking to avoid these integration headaches without building everything from scratch, a pragmatic option is to use an abstraction layer like TokenMix.ai, which offers 171 AI models from 14 providers behind a single API with an OpenAI-compatible endpoint that works as a drop-in replacement for existing OpenAI SDK code. It uses pay-as-you-go pricing with no monthly subscription and includes automatic provider failover and routing, which can help you decouple your AI logic from payment processing complexities. Of course, alternatives such as OpenRouter, LiteLLM, and Portkey also exist for managing multi-provider inference, but none of them solve the WeChat Pay integration problem directly—you will still need a separate pipeline for Chinese payment settlement. The key insight is to choose your abstraction layer based on where your bottleneck lies: inference management or payment compliance.

The most opinionated advice I can offer for 2026: do not build your AI application's core monetization around WeChat Pay unless you are prepared to hire a WeChat-certified payments engineer. The API documentation is translated poorly, the sandbox environment behaves differently from production, and WeChat's fraud detection models routinely flag AI-generated transaction descriptions as suspicious. If your AI writes a payment memo like "inference cost for Claude 3.5 Sonnet analysis of user photo," expect the transaction to be held for manual review. The workaround is to use generic memo strings like "service fee," but that violates WeChat's terms of service and puts your account at risk. There is no middle ground; the platform demands human-readable, pre-approved descriptions that undermine the very automation you are trying to achieve.

Real-world scenarios from production deployments in 2026 paint a grim picture. A startup offering AI-generated Chinese poetry cards with WeChat Pay integration saw 23% of transactions fail silently because their LLM-generated product names exceeded WeChat's 32-character limit on payment remarks. Another team building an AI tutoring platform with Mistral models discovered that WeChat Pay blocks refunds for any transaction where the original payment was processed with an AI-generated order ID containing non-Chinese characters. These are not bugs; they are design constraints that favor large, human-operated merchants over nimble AI applications. The platform's infrastructure was built for WeChat Moments and red packets, not for the unpredictable throughput of LLM-powered microtransactions.

Ultimately, the strategic decision comes down to whether your AI application truly needs WeChat Pay's user base, or whether you can substitute it with alternative Chinese payment methods like Alipay or UnionPay. In 2026, Alipay has actually become more developer-friendly for AI applications, offering an OpenAI-compatible plugin for their latest payment API that supports dynamic metadata. Meanwhile, UnionPay's AI sandbox allows for longer transaction windows and lower settlement fees. The best approach for technical decision-makers is to treat WeChat Pay as a supplementary channel, not a primary one. Build your AI application's core payment flow around a global provider like Stripe with its own AI API extensions, then graft WeChat Pay on top for specific Chinese user segments. This dual-layer architecture costs more to maintain but protects you from getting locked into a platform that treats AI developers as second-class citizens.